Big Five Clouds Won’t Admit $20B AI Capex Cut for Weak Demand

My call: None of the Big Five will publicly slash $20B+ of AI capex for “weak demand” before 2028.

Are Hyperscalers About to Admit They Overbuilt the AI Future?

Prediction Desk | Niles Overton

My call: No $20B AI walk of shame by 2027

Everyone is waiting for the same scene. A Big Tech CFO steps to the mic, clears their throat, and says the quiet part out loud: “We spent too much on AI data centers. Customers are not here for it. We are cutting twenty billion dollars.”

My call: that scene does not happen before December 31, 2027, for any of the Big Five U.S. cloud providers. Not Microsoft, not Amazon/AWS, not Alphabet/Google Cloud, not Meta, not Oracle.

They might slow builds, reshuffle regions, or quietly push projects into 2028 and beyond. They will blame power grids, permits, and “prioritization.” What they will not do is put a big round number on the table and say, in plain English, that weak AI demand forced a $20B reversal.

The trillion‑dollar comfort object

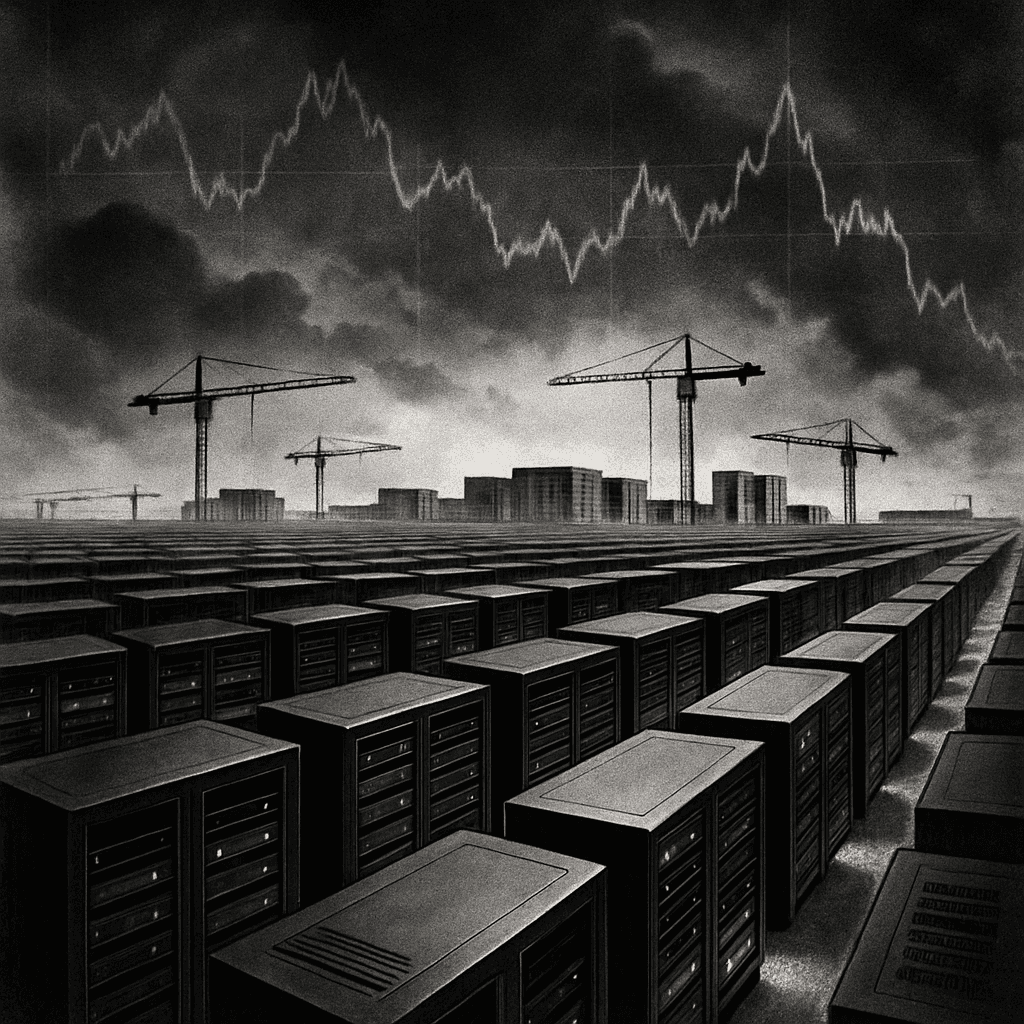

Goldman pegs AI‑driven data‑center capex at $7.6 trillion through 2031. That is not a business plan, it is a group therapy exercise for boardrooms that need to believe the next decade has a script.

The awkward part: early revenue is not keeping up with the mood board. Enterprises are still piloting copilots. Productivity gains are more slideware than P&L. CBS quoted analysts pointing out the obvious: the returns are not matching the rhetoric, even as hyperscalers tap debt markets to keep the shovels moving.

Yet this exact mismatch is why a clean $20B “demand is weak” cut is unlikely. AI capex has graduated from normal product budgeting to national strategy, executive ego, and stock‑multiple maintenance. Once your valuation and your geopolitical pitch are welded to the AI narrative, you treat capex like nuclear deterrence: regrettable, expensive, and non‑negotiable in public.

How to overbuild without ever saying you overbuilt

The Big Five do not need AI demand to match the hype by 2027. They only need it to be ambiguous enough that they can keep talking about “long‑term opportunity” while accountants quietly fix the gap.

That is where the real driver sits: they have better stories available than “customers are not buying this.” Any serious capex wobble will be framed as one of three things.

First, power and permits. U.S. grid headroom is forecast to go red around 2027. That is a gift to anyone who wants to slow a build without spooking the AI narrative. You do not say “no one wants to pay for this inference cluster.” You say “we are re‑sequencing deployments due to transmission constraints and our commitment to clean energy.” Somewhere, a project manager quietly thanks NERC for making their life easier.

Second, “optimization.” Utilization on GPUs looks soft? Training workloads slip? Fine. You tell investors you are shifting from low‑return training to higher‑margin inference, from generic capacity to “targeted, customer‑driven builds,” from on‑grid to behind‑the‑meter. You brag about efficiency and unit economics. The fact that this also involves spending less, later, in some places is treated as a happy byproduct of operational excellence.

Third, geography. If demand is squishy in one region, they will move capex, not erase it. India is throwing out incentives like festival sweets. Amazon talks up a $48B India plan. Microsoft and Google are right behind. If U.S. regulators or ratepayers turn hostile, a hyperscaler can trim a North American campus and quietly make it up with a new “AI hub” where the tax breaks are generous and the questions are few.

Each of those moves can easily sum to more than $20B over several years. None of them requires a press release that reads “we misjudged demand.”

The market wants a confession, the incentives want a script

Investors are starting to ask the right question: what if the trillion‑dollar AI capex supercycle produces something closer to a respectable business than a new internet? The Nasdaq’s AI jitters are not about philosophy, they are about cash flow.

But look at the other side of the table. AI is no longer a side bet that can be trimmed to appease a cranky quarter. It is the story that justifies why these companies get to trade at premium multiples, anchor national AI strategies, and fly CEOs to summits about the fate of civilization. You cannot walk into that room and say “actually, uptake is a bit soft so we are cutting $20B of the future.”

So they will do what any rational management team does in a hype‑sensitive sector:

- Spread the pain into a dozen small guidance tweaks instead of one big reversal.

- Blend AI capex into broader “cloud infrastructure” so it is harder to score who cut what.

- Let projects drift past 2027 and call it “phasing” or “portfolio discipline.”

This is not fraud. It is the standard art of not making yourself the poster child for an AI bubble while you still hope demand catches up.

What could break the script?

For my bet to fail, we need a real crack‑up. Not just softer enthusiasm, but a combination of brutal price wars, chronically idle GPU farms, and capital markets that stop rewarding any sentence containing the word “model.”

Then add a weak link. Think Meta or Oracle, players without the same diversified cash gushers that Microsoft and Alphabet enjoy. If one of them ends up over‑levered, under‑utilized, and under activist attack, the easiest way to reset credibility might be a very public AI pullback: a quantified $20B cut, with explicit language about slower‑than‑expected demand.

This is the “capex crack‑up” scenario. It is not impossible. It is just asking a lot of reality by 2027: global AI disappointment, tighter credit, and a management team willing to torch its own narrative instead of hiding behind grid maps and the word optimization.

How to score this bet

The resolution bar is deliberately high. To falsify this column, we would need a Big Five provider to do all of the following before December 31, 2027:

Publicly quantify a cut, cancellation, or multi‑year deferral worth at least $20B of previously articulated AI or data‑center capex, and explicitly flag weak or slower‑than‑expected AI customer demand as a primary reason. Not just transmission delays. Not just “reprioritizing for efficiency.” Demand has to walk into the sentence wearing a name tag.

Anything short of that, and we are in the world I expect: lots of careful language about pacing, plenty of quiet spreadsheet surgery, and no smoking‑gun admission that the AI arms race overshot the customer.

The satirical verdict

AI demand may or may not justify a $7.6 trillion concrete monument by 2031. What I am betting on is simpler: by the end of 2027, hyperscalers still prefer overbuilt data centers to underbuilt narratives.

So if you are waiting for a $20B AI capex confession, do not hold your breath. The only thing these companies will admit to over‑building this decade is expectations.

Around the Shallot

Stay in the same broken universe.

Forecasts, satire, cartoons, and quizzes should feel like one publication, not disconnected tabs.

Tech

DOGE Unveils ‘War UX 2.0’: U.S.–Iran Conflict To Be Managed Like A Buggy App Update

Department of Government Efficiency reassures public that if the ceasefire can’t be fixed, it can at least be A/B tested, monetized, and pushed to the cloud.

Jul 13

Forecast

By Mid‑August 2026, Iran Will Reopen Hormuz Oil Traffic

Iran says the Strait of Hormuz is shut until the U.S. leaves the neighborhood. Tanker traffic and mediators say something more boring: this is a price‑setting tantrum that ends in a technical deal, not a 90‑day blockade.

Jul 12

Comments

Be the first to comment.