Big Three Banks Will Post Another AI Fueled Trading Revenue Record

My call: Yes. JPMorgan, Goldman, and Bank of America will set a new combined equity‑trading record at least once before Q2 2027, still riding the AI wave.

My call: the “AI super‑cycle peak” discourse is early. JPMorgan, Goldman Sachs, and Bank of America will beat this quarter’s combined equity‑trading record at least once before Q2 2027, and they will still be bragging about AI when it happens.

Goldman just printed the highest stock‑trading revenue any bank has ever reported. JPMorgan and Bank of America posted equity‑trading jumps so rude they made analysts look like they forgot how to use Excel. Everyone then got on the earnings calls and said two things at once: this is a multiyear AI capex boom, and also markets are “close to as good as it gets.”

Those cannot both be true. I am siding with the part of the story that involves more fees.

The Scorable Bet

Here is the bet in plain English, so you can throw it back at me later.

Between now and the results for Q2 2027, at least one quarter will show combined equity‑trading revenues at JPMorgan, Goldman Sachs, and Bank of America above today’s record. In that same quarter, at least one of those banks will explicitly credit AI‑related deal flow or AI‑driven trading and hedging as a primary reason their equities line blew out.

If we get to Q2 2027 and this quarter is still the high‑water mark, I am wrong. No “normalized for FX,” no “excluding token costs.” Just the reported equities trading lines in the filings and the earnings scripts.

Why The Peak Narrative Is Wrong

The consensus comfort object right now is that this was a perfect storm that will not repeat: SpaceX IPO, Alphabet’s $90 billion stock sale, AI names whipping around, Asia piling into the trade, and a macro backdrop so benign Jamie Dimon felt moved to jinx it on live audio.

The problem with the “perfect storm” story is that storms are rare. This is construction season.

First driver: AI is an infrastructure story, not just a momentum story. Data centers, power plants, grid upgrades, semiconductor capacity in South Korea and Taiwan, even the odd utility deal in Florida, all need to be financed. That means repeat equity and equity‑linked issuance, plus the hedges, options, and structured products that live downstream of every jumbo deal.

Goldman’s David Solomon is not calling this a “multiyear AI capex super‑cycle” because he enjoys inviting regulator questions. He can see the pipeline. So can JPMorgan’s Jeremy Barnum, who described the environment as “downstream of the AI theme writ large on a global basis.” Translation: this quarter is version 1.0, not the patch notes.

Second driver: Volatility pays these desks in both directions. The bears say an AI correction will kill the party. The trading floors say, please, God, let it correct loudly. Crowded chip names and hyperscalers unwinding is not a revenue drought, it is a stress test with commissions. If the AI complex snaps twenty or thirty percent, the options desks do not go on vacation, they go on three phones at once.

In other words, the bull scenario and the messy‑correction scenario both give the big three multiple shots at a fatter quarter than this one. What they do not like is a flatline, and we are very far from everyone agreeing on what any AI leader is actually worth.

Third driver: AI is feeding geography, not just stock tickers. Bank of America is already talking about flows into South Korea, Taiwan, and Japan as investors hunt for semiconductor and AI exposure. Global broadening cuts two ways. It increases the chance that everyone blows up at once, but it also multiplies the number of desks, time zones, and products that can profit from the theme.

Record prints are a function of breadth as much as hype. Right now, the breadth is widening, not narrowing.

The Quiet Tailwind: Banks Are AI Users Too

There is a very online version of this story in which “AI Wall Street” is just a bunch of interns feeding ChatGPT to pick Nvidia price targets. Ignore that. The real internal AI work is much less glamorous and much more supportive of record quarters.

JPMorgan says it has nearly a thousand AI use cases live and spends close to twenty billion dollars a year on tech. That is not for vibes. It is for risk systems, client targeting, surveillance, and execution. If you can push more trades through the same human headcount and the same risk limits, your ceiling on record quarters is higher than it used to be.

Jamie Dimon himself has warned that many of these AI benefits will be commoditized. He is right, and that is precisely why it helps my bet. If most large banks get a cheaper, faster digital nervous system, then the industry capacity to process AI‑driven flow goes up across the board. When the next jumbo quarter hits, nobody will be stopping because the spreadsheets cannot keep up.

The catch is cost. Token and infrastructure bills will show up as a real P&L line item. That matters for margins. It matters much less for the single question we care about here: can the revenue line print a bigger number than last time at least once in the next three years.

What Could Make This Call Embarrassingly Wrong

You do not get to forecast without listing the banana peels.

The obvious one is a real macro accident. Hard recession, geopolitical shock that takes down risk appetite, or a policy misfire that nukes valuations and liquidity together. In that world, AI is just another growth theme that stopped trading because everyone sold their ETFs and went to cash.

The second is regulatory mood. If Washington or Basel decides that AI exuberance plus record trading profits equals systemic risk, they can kneecap equity trading with capital rules and model constraints faster than AI can auto‑draft the comment letters.

The third is competition. If the incremental AI flow leaks away to non‑bank market‑makers and electronic venues, the big three’s revenues can plateau while the pie keeps growing. The chips can hum, the data centers can glow, and yet the dealer take stays stuck below today’s peak.

Those are real risks. They are also blunt tools. To prevent a new record quarter across three global powerhouses for almost three years, the world has to stay both worse and tightly policed for quite a while. That is not the base case these banks are running, and for once, I am taking the same side of the trade.

How To Score This At Home

The resolution is simple enough to check without a Bloomberg terminal.

- Track the quarterly equity‑trading revenues JPMorgan, Goldman, and Bank of America report in their earnings releases.

- Add them up. If the combined number beats the current record in any quarter through Q2 2027, circle it.

- Read at least one of the earnings call transcripts or MD&A that quarter. If management clearly says AI‑related deals or AI‑driven trading and hedging were a main engine, the forecast pays out.

If we get through mid‑2027 with no new high, then this quarter was the mountain top and the AI super‑cycle branded merch goes in the clearance bin.

My money, metaphorically, is on at least one bigger spike. Wall Street has found a narrative that lets it collect record fees for financing the robots that are supposed to replace half its staff. It would be very out of character for the Street to peak on chapter one and roll the credits before the layoff memo hits send.

Around the Shallot

Stay in the same broken universe.

Forecasts, satire, cartoons, and quizzes should feel like one publication, not disconnected tabs.

Politics

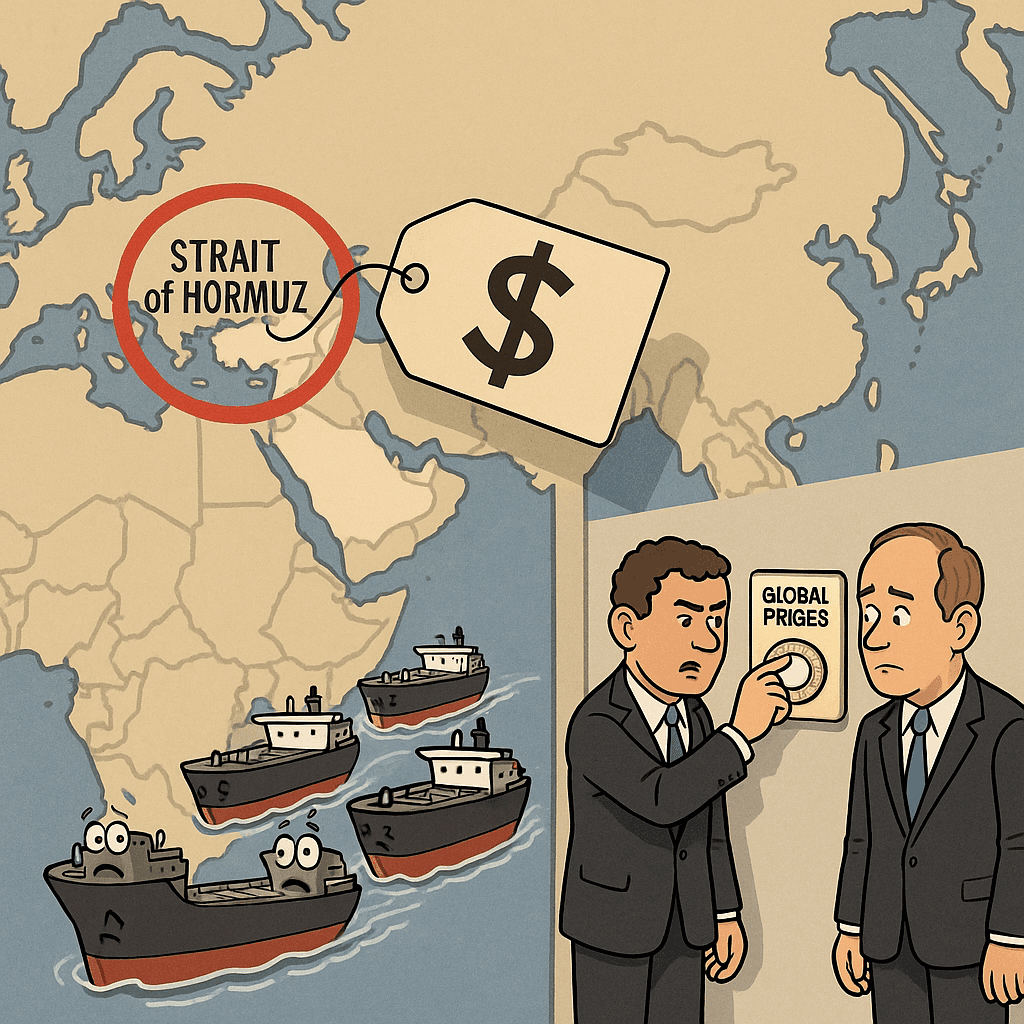

White House Launches ‘Surge Pricing for Stability’ Across Global Shipping Lanes

As tankers flee the Strait of Hormuz, U.S. officials reassure markets that chaos will be carefully monetized.

Jul 16

Forecast

Trump’s Hormuz Blockade Will Hold; His 20% Shipping Toll Won’t

Trump can keep U.S. warships turning back Iran’s tankers for two more months. Turning a Truth Social boast into a functioning global protection racket is the part that breaks.

Jul 14

Comments

Be the first to comment.