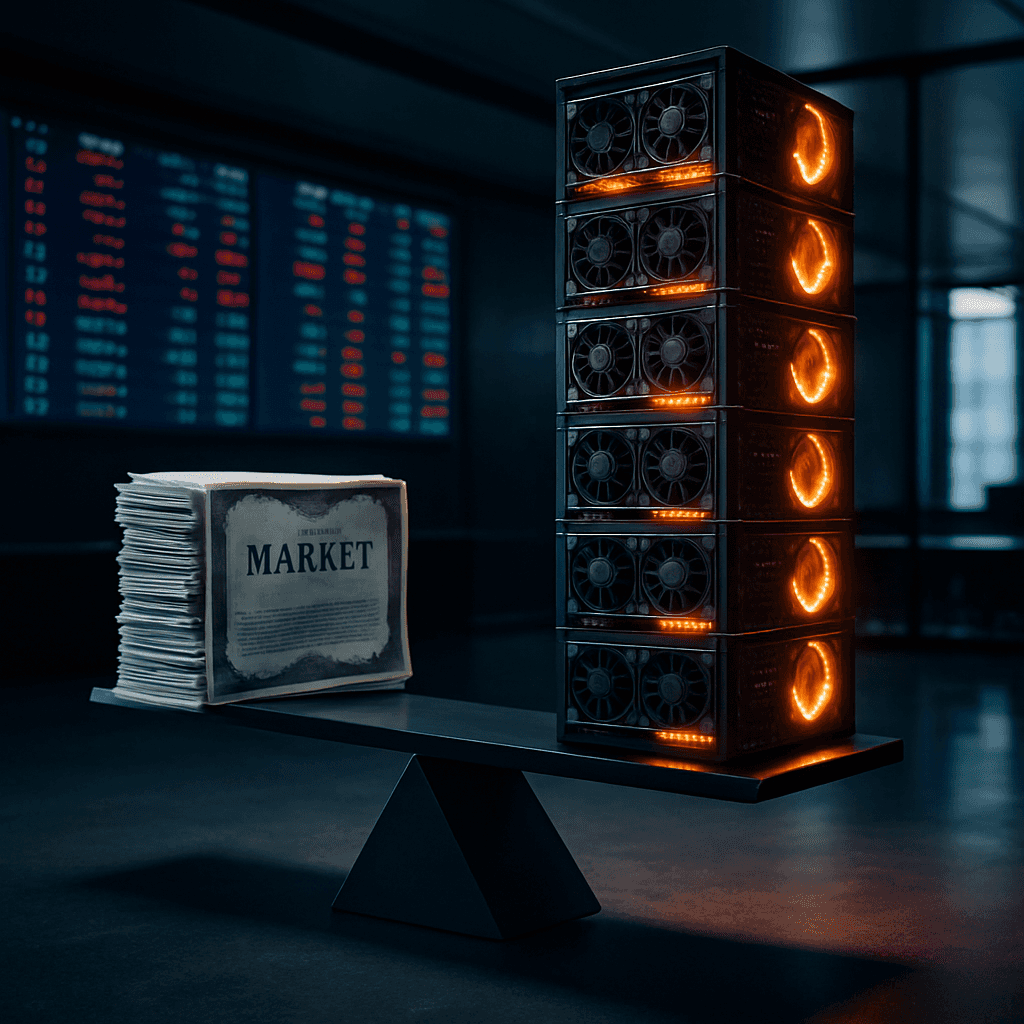

AI Leaders Will Not Beat The S&P By 20 Points

AI heavyweights should still post strong results, but their stocks are unlikely to sprint another 20 percentage points ahead of the broader market in just four months.

AI is now treated as the one trade investors cannot afford to miss.

Nvidia mints money. Micron, SK Hynix, and Samsung ride a memory boom that looks like a cheat code. Meta signs a $27 billion compute pact with Nebius, Nvidia tosses in $2 billion more, and a growing club of trillion dollar companies tells you that chips are the new oil, gold, and religion all at once.

Here is the call: over the next roughly 120 days, the AI trade does not beat the S&P 500 by another 20 percentage points. The boom does not die. It just stops being a license to print relative returns.

The Scorable Bet

Let us define the game in plain English so we can grade it later.

The bet: Take a simple AI basket, equally or value weighted, built from Nvidia, Micron, SK Hynix, Samsung Electronics, and the hyperscalers whose earnings are most loudly stapled to AI (Microsoft, Alphabet, Meta). Compare its total return to the S&P 500 Total Return index over the next ~120 days.

If that AI basket is more than 20 percentage points ahead by then, I am wrong. If it is under +20%, including outright underperformance, I am right.

This is not a call that AI is fake, that earnings roll over, or that a dot com style crash is inevitable by Halloween. It is a call that after one of the most violent re ratings in market history, the bar for another huge relative beat is now very high.

Why The AI Rocket Levels Off

The consensus story is simple. AI is the new electricity. Earnings are gigantic. Goldman says roughly half of expected S&P earnings growth this year comes from companies feasting on AI infrastructure buildout. CIOs go on CNBC to say the surge is justified by earnings and that productivity will eventually spread to the real economy like confetti.

They are not wrong on the direction. They are just extrapolating a sprint into a marathon.

Driver one: valuation and expectations. The AI complex is already priced for warpspeed. Magnificent 7 style earnings beats running north of 30 percent versus estimates are now the baseline. Each quarter that piles on makes the next quarter's hurdle higher. When everyone agrees Nvidia is a money machine, beating by another huge margin stops re rating the stock and just keeps it expensive.

Driver two: crowding and fragility. AI is now the world's favorite must own theme. AI ETFs, chip funds, and anything with a half convincing narrative have hoovered up flows. Korea's KOSPI, up nearly 90 percent in a year and trading like a bitcoin sidechain, shows what happens when an entire market becomes a levered bet on AI chips. That kind of price action is fun on the way up and vicious when someone finally reaches for the sell button.

Driver three: macro is not playing along. The Iran war hangs over energy supply. Oil spikes are not great for high multiple growth. Inflation is still annoying enough that futures traders see a real chance of the Fed hiking again, not cutting. Ten year yields do not need to soar for AI to wobble. They just need to stay uncomfortably high while everyone is priced as if discount rates soon drift back to 2021.

Driver four: breadth wants a turn. Even the AI bulls on TV are now talking about catch up from the rest of the market once war and inflation worries ease. If cyclicals and financials finally get to join the party, the S&P 500 can do quite nicely without AI leaders printing another heroic relative win. That alone kneecaps the odds of a clean +20 point gap.

Put together, the more likely path is that AI names keep out earning the pack but move from hyperdrive to cruise control. Very good is not the same as +20 percent better.

What Could Prove This Wrong

The meltup scenario is real. You can sketch it easily.

- Nvidia and friends keep smashing numbers, because demand for GPUs, memory, and data centers still outstrips even aggressive forecasts.

- Hyperscaler capex stays in money is a social construct mode. Deals like Meta Nebius and Nvidia's investment in Nebius become the norm, not the headline exception.

- Yields quietly drift lower, the Iran war deescalates, oil retraces, and the June Fed meeting delivers soothing ambiguity instead of hawkish resolve.

- Non AI sectors still lag because the real economy never quite convinces anyone, so passive flows and FOMO concentrate even more into AI mega caps.

This version of the world gives the AI complex one more parabolic leg, plus another 20 points of relative outperformance on top. If you believe in that full cocktail, you are effectively betting that fundamentals, flows, and macro all line up perfectly again for four straight months after one of the best runs in market history.

I do not. I think we get something messier. Still strong earnings, still big capex, but more day after hangover than fresh rally keg.

Signals To Watch While Everyone Argues On X

If you want to track this call in real time instead of checking back in 120 days with a told you so, a few dashboards matter.

First, earnings surprises and guidance from Nvidia, Micron, SK Hynix, Samsung, Microsoft, Alphabet, Meta. Are the beats still huge, or merely normal? Does anyone, in any footnote, hint that AI demand is powerful but not infinite?

Second, valuation spreads. Watch forward P/E and EV/EBITDA for a decent AI basket versus the S&P 500. If that premium widens meaningfully from here, the meltup case is back in play. If it stalls or compresses, that is my thesis working.

Third, breadth and flows. Are more S&P names finally trading above their 50 and 200 day moving averages, or is it still the same ten tickers dragging the index uphill? Do AI branded ETFs keep hoovering money, or do some of those flows discover the radical asset class known as anything else?

Finally, macro pressure. Keep an eye on the 10 year yield, Fed funds futures, and oil. High valuations can survive scary headlines or higher discount rates, but not usually both at once.

The Satirical Verdict

This is a forecast, not a sermon. I am not telling you to short the robots. I am saying that a trade which has already pulled a decade of hype into a couple of years now has to clear a visibly absurd bar to keep humiliating the rest of the market.

My money, figuratively, is on the AI complex delivering solid absolute gains, strong earnings, and a mere mid teens relative edge at best. The boom matures. The S&P's non AI peasants get a small raise. Korea discovers gravity. The word bubble gets downgraded to expensive but fine.

If I am wrong, and the AI basket smokes the index by another 20 percentage points before the leaves turn, we will know what kind of supercycle we are really in. Not an earnings supercycle, but a self inflicted one in which the global financial system has been permanently reprogrammed to buy anything that looks like a GPU rack in a hoodie.

Around the Shallot

Stay in the same broken universe.

Forecasts, satire, cartoons, and quizzes should feel like one publication, not disconnected tabs.

Tech

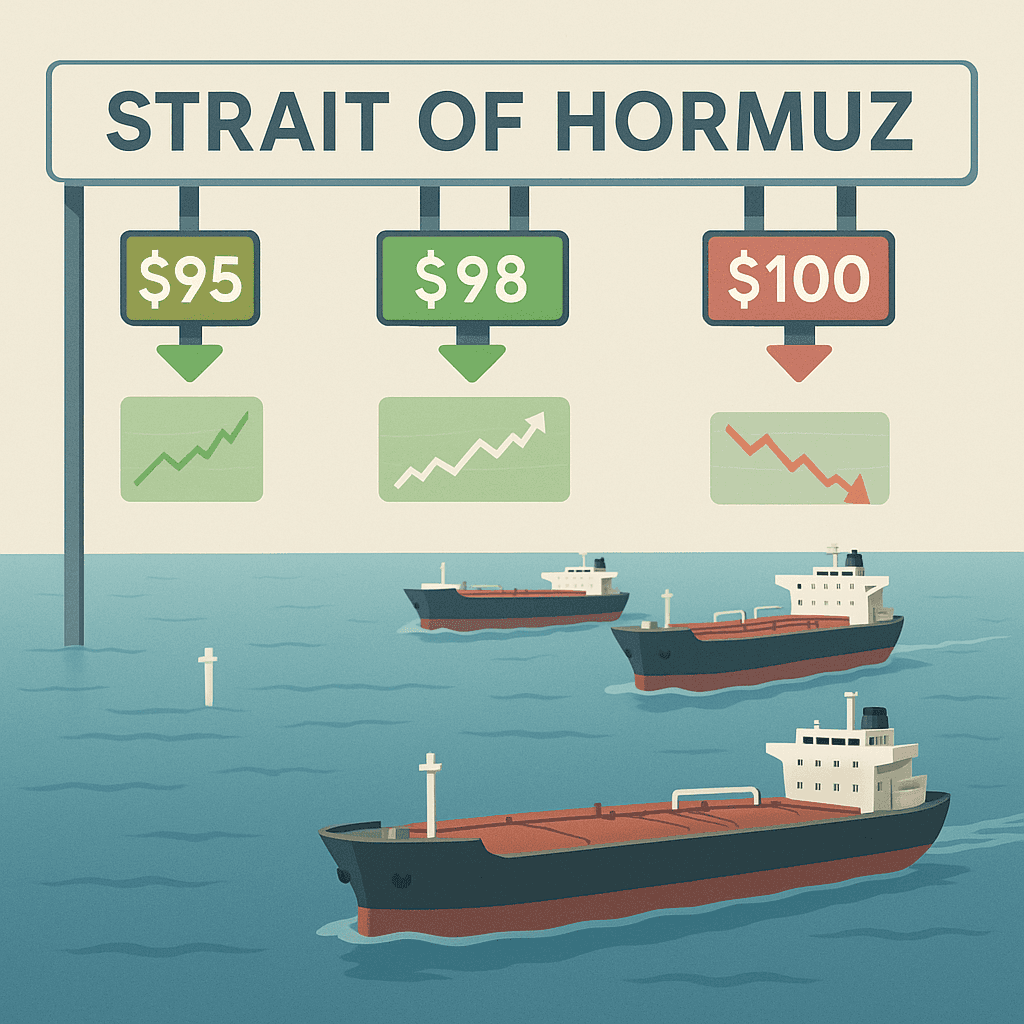

Trump Unveils ‘War-as-a-Service’ Pricing: $100 Oil, Optional Democracy Add‑On

Blockade 2.0 rolls out in the Strait of Hormuz as markets crash, gas spikes, and everyone pretends this is still about “deterrence” and not revenue per barrel.

Jul 14

Forecast

Trump’s Hormuz Blockade Will Hold; His 20% Shipping Toll Won’t

Trump can keep U.S. warships turning back Iran’s tankers for two more months. Turning a Truth Social boast into a functioning global protection racket is the part that breaks.

Jul 14

Comments

Be the first to comment.