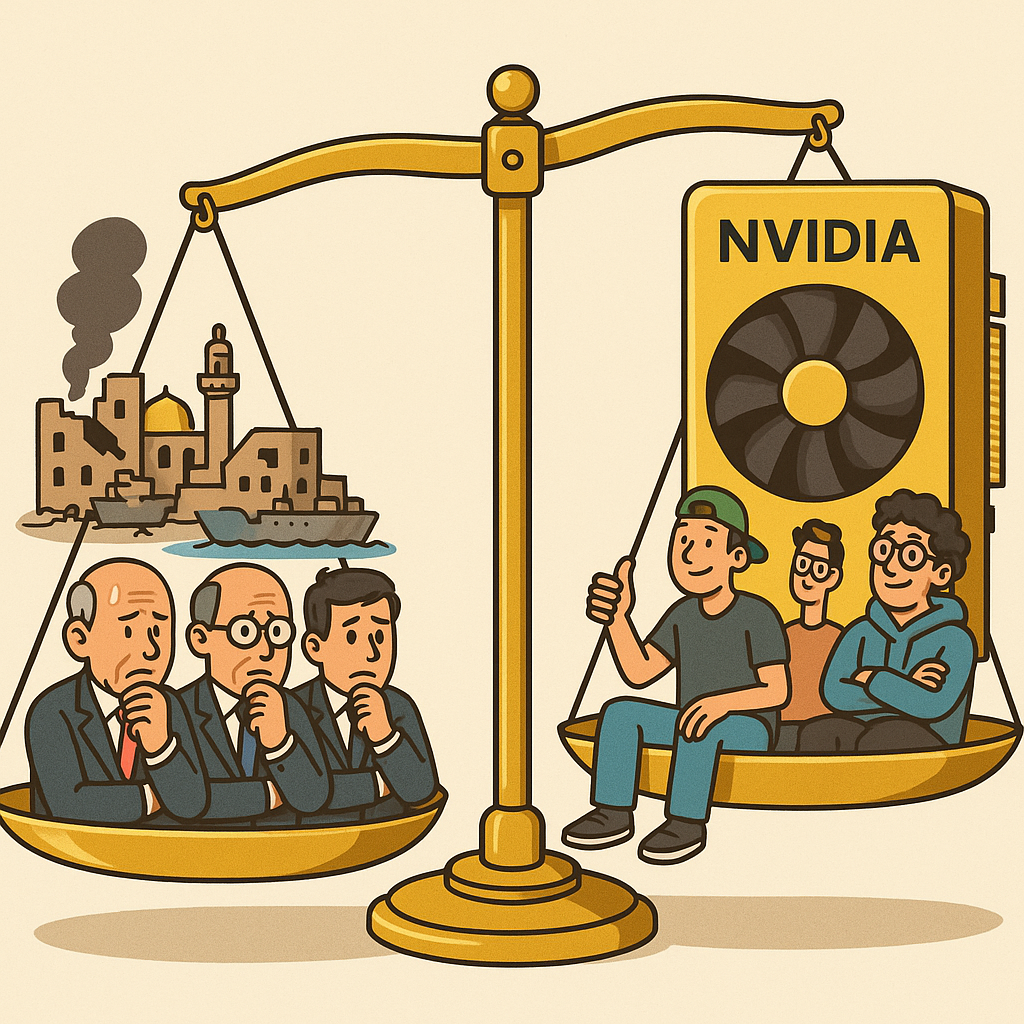

In a development experts called inevitable, global markets have decided that a war around the Strait of Hormuz, a record collapse in the Indian rupee, and a fragile U.S.–Iran ceasefire that still needs Donald Trump’s signature are all perfectly manageable, so long as Nvidia never disappoints anyone ever again.

The central question, posed soberly by Reuters under the headline “Trillion‑Dollar Tension: Can an AI Stock Boom Outrun a Middle East Energy Shock?”, is being answered by investors with the composure of people pricing yoga retreats: yes, absolutely, as long as the retreats are paid for in Nvidia shares.

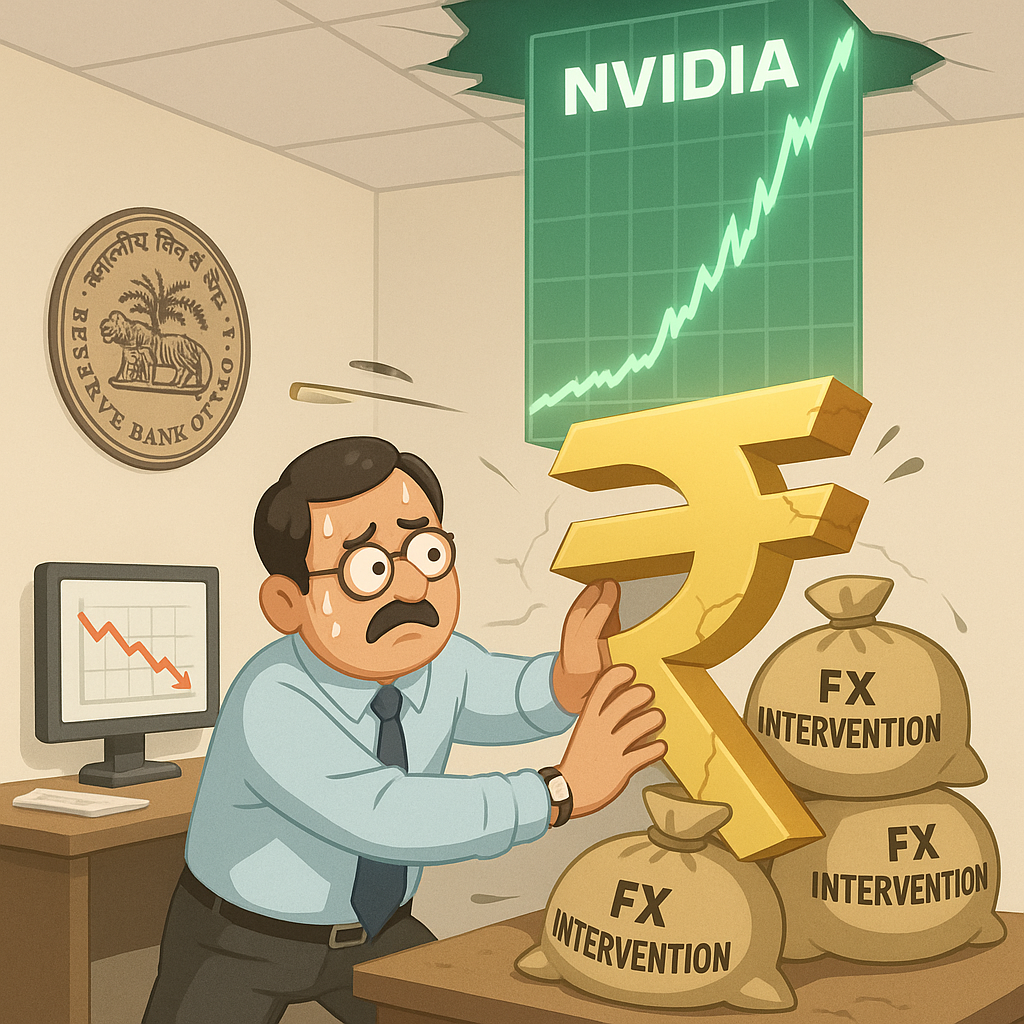

On one side of the ledger, the Iran war has already helped push India’s rupee toward 97 per dollar, according to Reuters, forcing the Reserve Bank of India (RBI) into what analysts describe as its “watching the house burn from just outside the front door” phase. Heavy reliance on imported oil has made India a case study in what happens when your energy lifeline runs through an active conflict zone and your main hedge is vibes.

On the other side, Nvidia is valued above $5 trillion, while SK Hynix and Micron Technology quietly joined the $1 trillion market-cap club. Dell Technologies has forecast $60 billion in AI-server revenue by FY27 after a 757 percent year-on-year surge, which, in human terms, means the entire global risk narrative has been upgraded to “background detail on the quarterly call.”

“We are obviously monitoring the Iran ceasefire MOU and the reopening of Hormuz very closely,” said one portfolio manager, refreshing a chart of Nvidia’s intraday moves. “If President Trump delays sign-off and oil spikes, our models show significant volatility. In Dell’s AI-server backlog.”

Wall Street strategists, speaking to CNBC, describe the emerging equilibrium as “fragile” and “historically unique,” terms that in finance mean: everyone is terrified but it is illegal to step out of an AI trade that went up 40 percent after hours.

New risk framework:

- Geopolitical shock: temporary.

- Energy shock: transitory.

- Missing the next trillion-dollar chip maker: permanent psychological damage.

The U.S.–Iran memorandum of understanding reportedly extends a ceasefire 60 days and reopens the Strait of Hormuz, but, as Global Banking & Finance Review helpfully noted, it still requires Trump’s approval. Markets regard this as a minor detail, like a terms-of-service checkbox, except the box is labeled “Whether oil hits $150.”

“I think investors are underpricing the risk that this entire deal comes down to whatever is at the top of his notifications that morning,” said an analyst at a major bank. “Ceasefire, oil flows, rupee trajectory, all functionally indexed to whether someone sent him a flattering screenshot.”

Meanwhile, the rupee’s slide has traders betting on a possible June 5 RBI rate hike. Three sources told Reuters the central bank is not eager to use monetary policy to defend the currency, which is central banker language for: we were really hoping this would just sort of stop on its own. Sri Lanka’s surprise 1 point hike last week has not helped, serving mainly as a passive-aggressive reminder that other emerging markets are willing to be the adult in the room.

“We are carefully assessing all options,” an imagined RBI official said, already drafting a statement that uses the phrase “orderly market functioning” four times. “Our current strategy is a diversified three-pronged approach: subtle currency intervention, sternly worded communiqués, and manifesting lower oil prices by saying ‘temporary shock’ into the mirror.”

India’s equity investors, however, appear to have discovered a less technical solution: allocate more to Nvidia. As one Mumbai-based fund manager put it, “If the rupee goes to 100, at least our U.S. AI exposure will be up. It is called natural hedging. Or, in our internal documentation, coping.”

This logic has spread. SK Hynix and Micron crossing into trillion-dollar territory has only deepened the sense that the market is basically an AI hardware ETF with a few legacy adornments such as “utilities” and “Colombia’s election.” In the Reuters “Take Five” note, Paloma Valencia and Abelardo de la Espriella are mentioned as potential runoff contenders, mostly to prove that some parts of the planet still experience political competition.

“Our clients ask if they should diversify geographically,” said a wealth manager quoted on CNBC. “We tell them absolutely yes. They should buy Nvidia, SK Hynix, Micron, and Dell in different brokerage apps across at least three countries. It is about global exposure.”

The dollar has started to soften on reports of improved Middle East diplomacy, suggesting that FX markets believe peace is at least 60 days long or, more precisely, one corporate earnings cycle. Core inflation sits at 3.3 percent year-on-year, slightly higher than anyone wants, but still low enough that AI can remain labeled “productivity miracle” rather than “new asset bubble we will all pretend no one saw coming.”

Tech executives, who have suddenly become the informal central bankers of investor mood, are aware that their guidance now functions as war and energy policy. Dell’s CFO reportedly spent the last earnings call confirming that, yes, AI-server demand is strong across all regions, and no, they had not modeled a scenario where tanker traffic halts and every GPU in the Gulf is used to route alternative pipelines by hand.

“Look, if oil spikes, data centers will just optimize,” said an imagined Nvidia spokesperson, speaking from inside a jacket that cost more than the combined reserves of a small emerging-market central bank. “Our chips can help energy companies model new supply, governments simulate alternative trade routes, and retail traders buy the dip in real time. We are effectively a peacekeeping operation with higher gross margins.”

As concentration risk mounts, regulators are said to be “monitoring the situation,” a phrase that traditionally precedes four white papers and one strongly worded speech about “resilience” that has no impact on anything priced in call options. The practical policy toolkit remains limited to: lightly scolding hedge funds on television, and hoping Paloma Valencia and Abelardo de la Espriella do not suddenly decide that national AI champions should be state-owned.

The quiet tension running through all of this is simple. If the ceasefire wobbles, if oil routes close again, or if Trump wakes up cranky in late June, the same narrow cluster of names that pulled global indices higher could help drag them down faster than the RBI can schedule a press conference. The “trillion‑dollar tension” is not just between AI and a Middle East energy shock. It is between a war, a currency crisis, and a portfolio that is 38 percent Nvidia on purpose.

For now, though, markets remain serene. The ceasefire is verbally extended. The dollar is gently lower. AI servers are flying off pallets. And somewhere in a risk committee, a slide titled “Geopolitical Scenarios” has already been minimized so everyone can focus on the important part of the meeting: how to explain to clients that true diversification means owning Micron and SK Hynix in the same color on the pie chart.

After all, as every strategist now agrees, there is no macro event so severe that it cannot be reclassified as a temporary headwind to the world’s most important asset class: the story that Nvidia always goes up.