In a development experts called inevitable, markets have decided that rockets, low-Earth orbit routers, and one man’s Mars fan fiction are collectively worth more than the GDP of Canada and roughly three entire German car industries stacked in a trench coat.

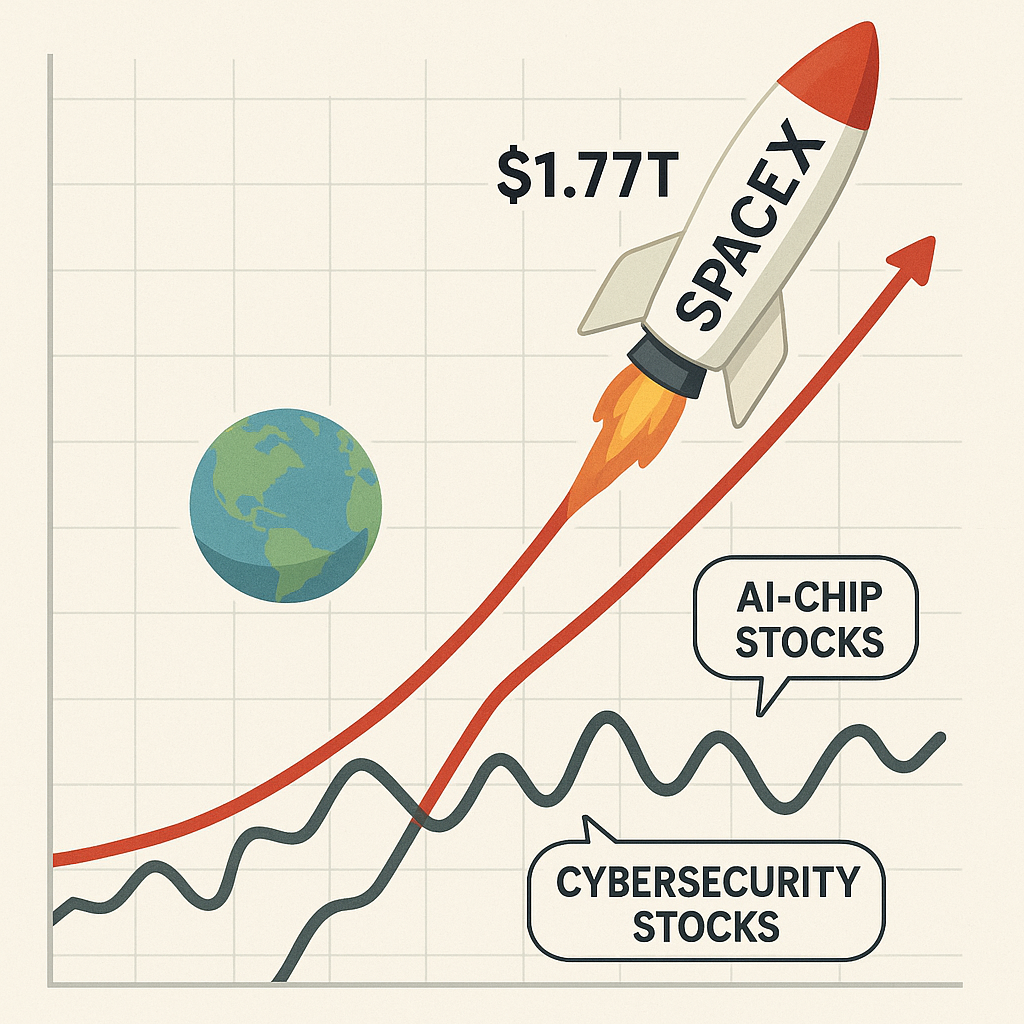

SpaceX, which according to CNBC has fixed its IPO price at 135 dollars a share to raise 75 billion dollars, will debut at an implied 1.77 trillion dollar valuation, instantly entering the S&P 500’s platinum loyalty tier. The number slots SpaceX as the seventh-largest U.S. company and, more importantly, as the first firm whose fundamentals are modeled primarily in units of “vibe-adjusted optimism per launch.”

“We look at launch cadence, Starlink ARPU, and the unpriced optionality of fleeing this planet if Broadcom guidance misses again,” said one tech strategist at a major bank, speaking on condition of anonymity because his price target is just an animated GIF of a Falcon 9 going up forever, carefully embedded in a 78-page PDF titled ‘Space as a Service.’

Broadcom itself, which just reported 48 percent year-over-year revenue growth on custom AI chips, saw its stock wobble after its outlook failed to meet the industry’s informal standard of ‘permanent vertical line.’ CrowdStrike beat earnings, announced a four-for-one stock split, and was punished with a 10 percent drop for the crime of existing in normal physics. Against this backdrop, investors greeted SpaceX’s 1.77 trillion dollar tag as a comforting return to basics: a simple story about strapping debt, satellites, and hopes for AI-fueled exports in Asia to the side of a reusable tube and lighting it on fire in front of a live-streamed countdown sponsored by three ETFs.

“Relative to AI names, this is actually easier to underwrite,” said Terry Duffy of CME Group, who recently warned CNBC that perpetual futures incite bad behavior. “With SpaceX, the perpetual futures are just called ‘Mars colony by 2040.’ From a risk standpoint, I almost prefer the rockets to an AI ETF that owns 40 identical chip charts and one yoga app.”

In early trading, U.S. tech futures slipped while oil prices fell on news of a Lebanon ceasefire and President Trump’s reported decision to only resume all-out war with Iran if Tehran kills American troops, according to the Wall Street Journal. Traders interpreted this grim conditional as a rare volatility hedge: as long as no one missteps, the only thing that can blow up their portfolio is the 555.6 million-share space IPO they just levered into on margin using a brokerage app that renders geopolitics as tiny color-coded rockets.

Elon Musk’s personal net worth could surge past 1 trillion dollars on a successful listing, a milestone wealth-tax advocates are already screen-printing onto tote bags. Senator Elizabeth Warren, who was on CNBC this morning discussing an AI tax and her two-cent wealth tax proposal, reportedly asked staff whether the IRS could accept Starlink terminals as in-kind payment or at least garnish a couple of low-Earth orbit slots.

“We have factory orders up 4.8 percent, an AI-export boom in Asia cushioning energy shocks, and one individual on track to become a trillionaire,” said a senior Hill staffer. “It is important to signal to voters that we are laser-focused on the real economy by holding a hearing about whether Elon can buy the moon and then lease it back as a data center.”

Inside the roadshow, SpaceX bankers framed the company as the missing infrastructure layer for an AI-driven planet. Data centers are straining national grids. Cables are vulnerable to sabotage. The solution, naturally, is to move the broadband choke point into orbit and lease spectrum, launches, and orbital real estate to whoever survives the next ceasefire cycle while still clearing compliance on export controls.

“Think of SpaceX as a toll road operator, except the road is the sky and the toll is global dependence,” one slide reportedly read, according to someone who claimed to have seen the deck and immediately tried to subscribe to it on an ETF basis the way normal people subscribe to a streaming service.

Earlier slides, according to the same attendee, modeled Starlink as a kind of planetary router of last resort, routing AI inference traffic around blackouts, fiber cuts, and the occasional sanctioned shipping lane. One footnote described geopolitical risk as “latency with flags.”

The pitch has found an eager audience among Asian exporters riding the AI boom. As CNBC noted, several economies in the region are leaning on AI-related exports to offset energy costs. For them, SpaceX is not just a stock, it is a latency hedge. If oil spikes on renewed Iran tensions and terrestrial shipping routes get dicey, at least your model checkpoints can still reach Iowa and your inference cluster in Singapore does not depend on whether a stray anchor finds the wrong cable.

“Our AI chip shipments cross three war-risk zones and two disgruntled navies,” said a Taiwan-based executive who requested anonymity. “Frankly we would prefer to fire them through a Falcon 9 like a t-shirt cannon and just insure the launch window instead of the Strait of Hormuz.”

Index providers are also preparing for impact. If the IPO trades well, benchmark-constrained funds will have to own SpaceX, regardless of whether they currently have an ‘interstellar logistics’ bucket. One passive-fund manager said his firm is prototyping a new allocation model that breaks the market into three sectors:

- AI enablers (Broadcom, Nvidia, data-center landlords)

- AI defenders (CrowdStrike, other cybersecurity firms tasked with stopping the enablers from being immediately stolen)

- Escape plans (SpaceX and, in a pinch, bunker REITs)

“The mix will depend on whether Congress actually reins in presidential war powers or just rebrands them as a premium DLC,” the manager said. “Right now the model assumes mild geopolitical chaos and aggressive multiple expansion for anything that can leave orbit or bury fiber under a private ranch in New Zealand.”

Corporate governance experts, who have spent a decade warning about Musk’s overlapping roles across Tesla, X, SpaceX, and various AI ventures, are quietly updating their threat models to include “trillionaire CEO with his own launch stack and global internet backbone.” Asked whether this concentration of power might invite new antitrust scrutiny, one regulator noted that the agency’s cloud task force currently has three staff members and a shared spreadsheet that still calls AI “emerging software.”

“We are watching developments closely,” the regulator said. “If he starts pricing Starlink in units of ‘judge-resistance bandwidth’ we may open a comment period and perhaps even hire a fourth person.”

For now, investors appear content to ignore both antitrust risk and physical war risk in favor of a cleaner narrative: SpaceX as the rational endpoint of a decade-long private space buildout. After all, launch revenue is real. Starlink subscribers are real. Government contracts are very real. The speculative part only kicks in when you try to reconcile those numbers with a valuation that assumes every future satellite, every Mars mission, and every congressional hearing about wealth inequality ends with the same outcome: the line keeps going up and geopolitics remains a helpful marketing slide.

This is where the AI bubble quietly reenters the chat. Broadcom’s wobble and CrowdStrike’s post-earnings drop remind traders that even AI infrastructure must eventually report earnings that map to Earth. SpaceX offers a new way out. If chips are overextended and software multiples are tired, perhaps the answer is to value the infrastructure that will carry the AI that will design the chips that will optimize the rockets that will launch more satellites that will carry the AI, a closed loop of optimism repeatedly inscribed onto quarterly decks.

At these levels, analysts say, you are no longer buying discounted cash flows. You are buying the comfort of knowing that when the next Iran headline hits, oil spikes, or a House resolution trims war powers by two percent, you own a slice of the only thing markets still trust more than AI itself.

Gravity, after all, has already been priced out and repackaged into a thematic ETF.